FEMA NDI

In exercise of the powers conferred under Section 46(2) (aa) and (ab) of the Foreign Exchange Management Act, 1999 and in supersession of the Foreign Exchange Management (Transfer of Issue of Security by a Person Resident outside India) Regulations, 2017 and the Foreign Exchange Management (Acquisition and Transfer of Immovable Property in India) Regulations, 2018, the Central Government issued Foreign Exchange Management (Non Debt Instruments) Rules, 2019

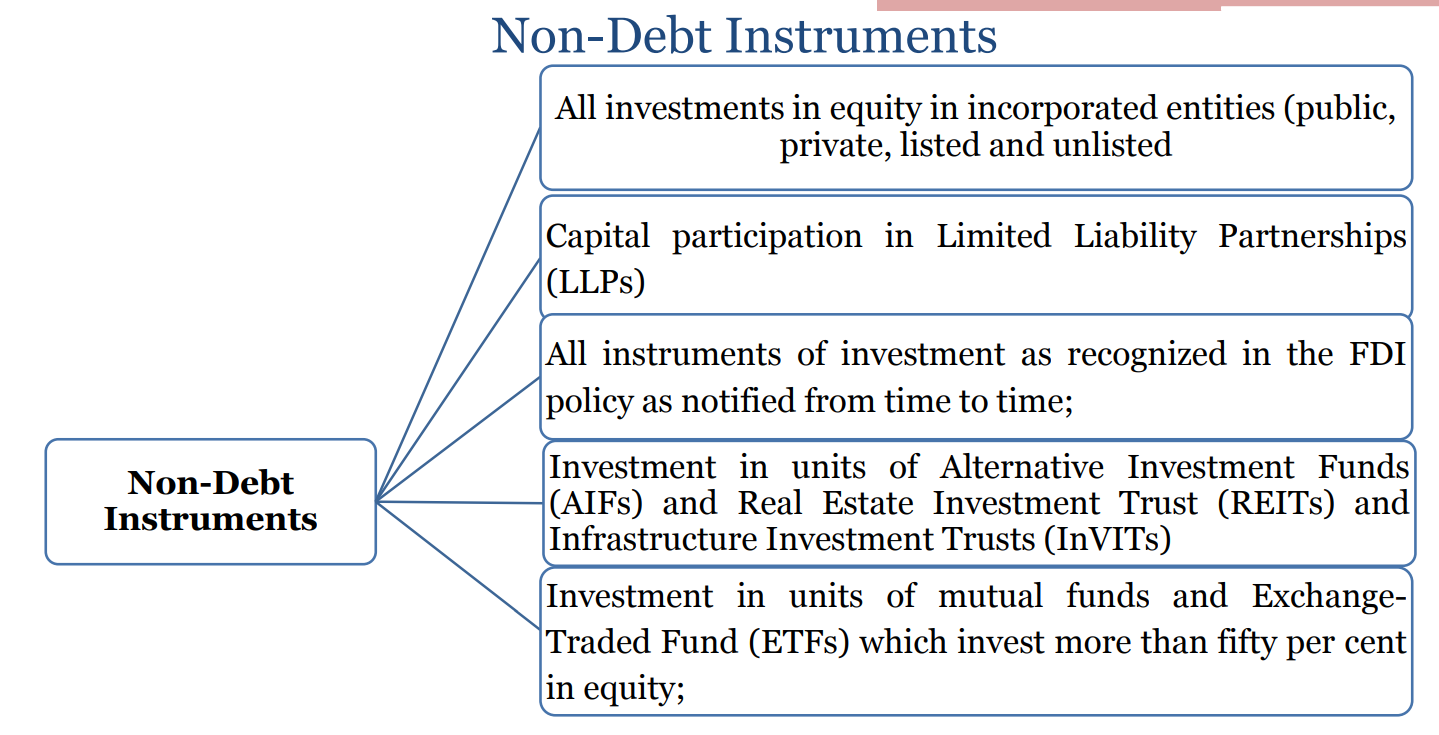

The legal framework for the administration of foreign exchange transactions containing Non debt instruments in India is provided by the of FEM(Non-debt Instruments) Rules, 2019

Recent amendment creating hurdles

The amendment to the Indian Foreign Exchange Management (Non-debt Instruments) Rules, 2019 (“FEMA NDI”), has posed a significant challenge for Indian companies, especially start-ups and smaller enterprises seeking foreign investments.

This amendment stipulates that any investments in Indian companies, whether direct or indirect, originating from entities located in countries that share land borders with India, or where the “beneficial owner” of the said Indian investment is situated in, or is a citizen of any of these Neighbouring Countries would necessitate prior government approval (“PN3 Requirement”).

While the aim of the amendment which was promulgated during the COVID-19 pandemic was salutary — i.e., to curb opportunistic takeovers or acquisitions of Indian companies by Neighbouring Countries during difficult times created by a black swan event — it created vast incertitude as the term ‘beneficial owner’ has not been explained or defined, and other laws that have a definition of the term are context-specific.

When the PN3 requirement was first introduced, the industry in general was comfortable taking a lenient view, relying on the beneficial ownership thresholds that were legislated in other laws.

But since the latter half of 2023, the Reserve Bank of India (RBI) has begun taking a more conservative view concerning issues on which the law was silent, especially under FEMA NDI.

The obstacle of navigating the prior government approval route is exacerbated by its time-consuming nature and high rejection rate.

With the PN3 Requirement, the onus of compliance is on the Indian company that receives foreign investment, with the regulatory authorities having the discretion to impose fines of up to three times the investment received.

The inherent vagueness within the legislation, along with severe penalties, can cast doubts on the survivability of these companies.

Many of these startups receive investments far beyond their revenue or assets. So, such fines could leave them insolvent, even if they liquidate.

Non-compliance would likely trigger legal battles, adding to India’s already significant backlog of court cases.

Way forward

Indian companies could consider having foreign investors to furnish representations backed by indemnities regarding their compliance with the PN3 Requirement. However, this may discourage foreign investment due to potential liabilities.

Therefore, there is a pressing need to amend the PN3 Requirement to define “beneficial owners” comprehensively, including ownership thresholds and control tests

The definition of ‘beneficial owner’ should specify a precise threshold for ascertaining beneficial ownership, potentially ranging from 10% (as provided under the Indian company law) to 25% (as recommended by the Financial Action Task Force).

The selection of the specific threshold can be customised to align with the government’s objective of scrutinising varying levels of foreign investment across different sectors.

Even with the clarification of control-conferring rights in the definition, some ambiguity may persist due to the skilful drafting of peculiar clauses in the charter documents.

To mitigate this issue, FEMA NDI, akin to Indian competition law, could be amended to incorporate a time-bound consultation mechanism with regulatory authorities, to determine whether specific clauses are control-conferring.

COMMENTS